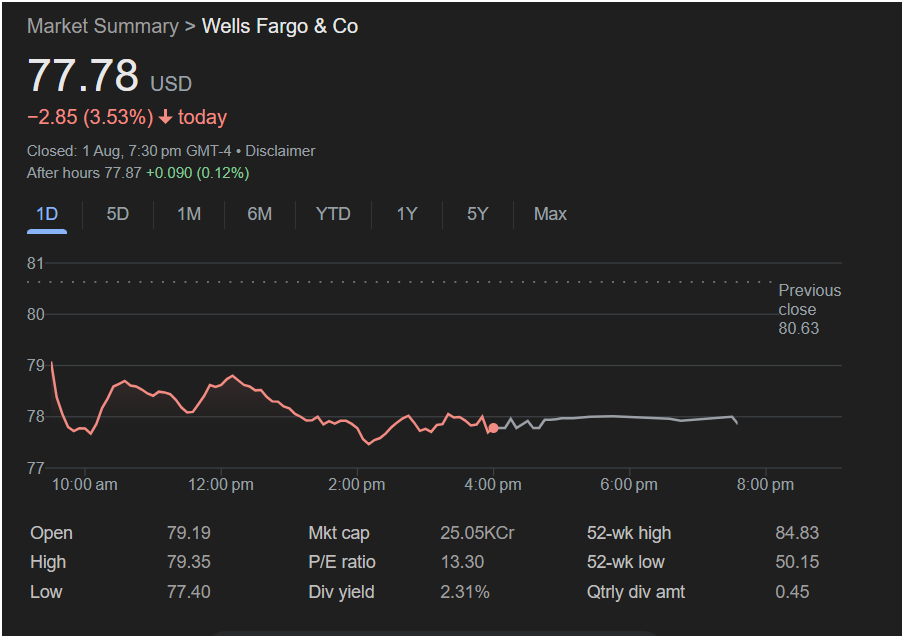

NEW YORK – August 3, 2025 — Shares of Wells Fargo & Co. (NYSE: WFC) slid sharply on Friday, closing down 3.53% at $77.78, as the banking giant faced investor unease tied to governance shifts and weakening macro indicators. The decline wiped out over $9 billion in market value in a single session, making Wells Fargo one of the day’s worst-performing financial stocks.

The stock opened weak at $79.19, well below Thursday’s close of $80.63, and touched an intraday low of $77.40 before staging a modest late-day rebound. The drop distances WFC further from its 52-week high of $84.83, although it still trades well above its low of $50.15. As of the latest trading session, Wells Fargo’s market cap stands at approximately $250.48 billion.[3][4]

CEO Charlie Scharf’s Chairmanship Sparks Governance Debate

CEO Charlie Scharf’s Chairmanship Sparks Governance Debate

The immediate catalyst for Friday’s downturn appears to be leadership developments at the top. The board’s decision to name CEO Charlie Scharf as the incoming Chairman — consolidating both roles — has drawn a mixed response. While intended to reflect confidence in Scharf’s stewardship, the move sparked concerns over corporate governance, particularly regarding board independence.[1]

Some governance advocates argue the decision reduces oversight, while others see it as a natural next step given Scharf’s multi-year effort to reshape the bank following its high-profile scandals earlier in the decade. The board’s new equity package for Scharf has also come under scrutiny from shareholder activists.[1]

Short Interest, Downgrade, and Outlook Cuts Add Pressure

Wells Fargo’s troubles aren’t isolated to leadership optics. A notable increase in short interest during July signaled that bearish sentiment was already building ahead of the latest news.[2] That caution was echoed by Phillip Securities, which downgraded WFC from “Buy” to “Accumulate”, citing valuation concerns and execution risk on forward guidance.[2]

That guidance, in turn, has become another sticking point. In mid-July, Wells Fargo cut its full-year net interest income (NII) forecast, projecting that 2025 results would be flat compared to 2024 — down from its previous estimate of 1% to 3% growth.[5][6][7] The revision was driven largely by pressure in the Markets business, which has struggled amid ongoing rate volatility and tighter liquidity conditions.

Dividend Hike and Q2 Earnings Offer Silver Linings

Amid the cloud of uncertainty, Wells Fargo offered some bright spots. In July, the bank raised its quarterly dividend by 12.5% to $0.45 per share, a move typically seen as a signal of confidence in future cash flows.[8][9] The dividend is payable on September 1, 2025, to shareholders of record as of August 8.[10]

Additionally, second-quarter earnings beat Wall Street expectations, driven by strong consumer banking activity and cost controls that helped offset softer trading income.[6][11]

Analysts Divided: Buy Ratings Persist, But Risks Remain

The analyst community remains split but cautiously optimistic. While some firms have adjusted their ratings, the overall consensus still leans “Buy” or “Moderate Buy”, reflecting confidence in Wells Fargo’s core franchises and capital strength.[12][13][14]

Recent price targets show a wide range, but the average hovers in the low-to-mid $80s. A set of 11 analysts recently pegged the mean 12-month target at $85.14, suggesting mild upside from current levels.[15][16]

However, analysts also warn of headwinds that could stall momentum — including lingering reputational issues, compliance scrutiny, and the uncertain trajectory of interest rate policy heading into Q4.

Investor Sentiment on Edge Ahead of October Earnings

Looking ahead, all eyes will be on Wells Fargo’s Q3 2025 earnings, set for October 14, as a key test of the bank’s ability to maintain profitability amid shifting economic conditions. Analysts and investors alike are parsing how the firm’s balance sheet will hold up if loan growth slows, or if deposit costs continue to eat into margins.

The interplay of factors — from governance shifts and short interest to dividend boosts and revenue mix — leaves the stock in a complex position as it approaches the fall. For now, Wells Fargo’s leadership may need more than boardroom confidence to restore momentum in a market that’s watching closely.

Let me know if you’d like this adapted for:

- Institutional investor briefings

- A newsletter digest format

- Or expanded into a deep-dive sector outlook covering peer banks like JPMorgan, Citi, and Bank of America

I can also provide visuals like stock chart comparisons, dividend yield trackers, or market cap shifts across the financial sector — just say the word.